On MS NOW’s Morning Joe today, Steve Rattner shows how June’s good inflation reading may be fleeting as the Iran War keeps pressure on oil prices.

Tuesday’s inflation reading came in a bit better than expected, but for individual Americans, the challenge of higher prices remains, in part because the renewed closure of the Strait of Hormuz has already started to push oil prices up again. And the persistent high inflation risks an increase in interest rates, as the new Federal Reserve chairman Kevin Warsh intimated in Congressional testimony this week. Among the few winners from the Iranian crisis has been the oil industry, whose profits and stock prices have been soaring.

Wednesday’s June inflation reading can be read two ways: Compared to May, prices declined because of the fall in oil (and derivatively, gasoline) prices. But compared to a year ago, prices were still 3.5% higher. That is the same amount by which wages are higher than a year ago, meaning that consumers have not achieved any “real” growth in the purchasing power over the past year.

Of course, those are averages and there is much data that shows how consumers further down the economic ladder are enduring more hardship than those at the top. For example, a recent study by the Federal Reserve Bank of New York found that higher income motorists have maintained their purchases of gasoline at roughly pre-war levels while those in the middle and – even more so – those further down have curbed their driving. Something similar happened when oil prices rose in 2022 due to the war in Ukraine, but the disparity is significantly greater this time around.

Gasoline prices rose in tandem with crude oil prices when the war started, but they have been coming down more slowly. Today, crude oil prices are about 18% above where they were at the end of February ($85 per barrel compared to $72 per barrel back then), but gasoline prices are 31% above where they were on February 27. That means the average price for a gallon of gas is $3.86 a gallon, compared to $2.94 per gallon before the war and a high of $4.50 a gallon.

Why is that? A mix of reasons. Speaking generally, prices sometimes “rise like a rocket and fall like a feather.” In other words, retailers try to hold the higher prices as long as possible. More specifically to the oil situation, inventories remain tight, particularly for refined products like gasoline, and refinery disruptions caused by the war have made it harder for oil companies to ramp up gasoline production.

But the oil companies have also been enjoying robust profits, which in turn has filtered through to their stock prices. An index of oil and gas companies is up nearly 28% this year, compared to less than 10% for the S&P 500 and just 2.7% for the “magnificent 7” technology companies. Meanwhile, the average worker’s wages are up just 1.3%.

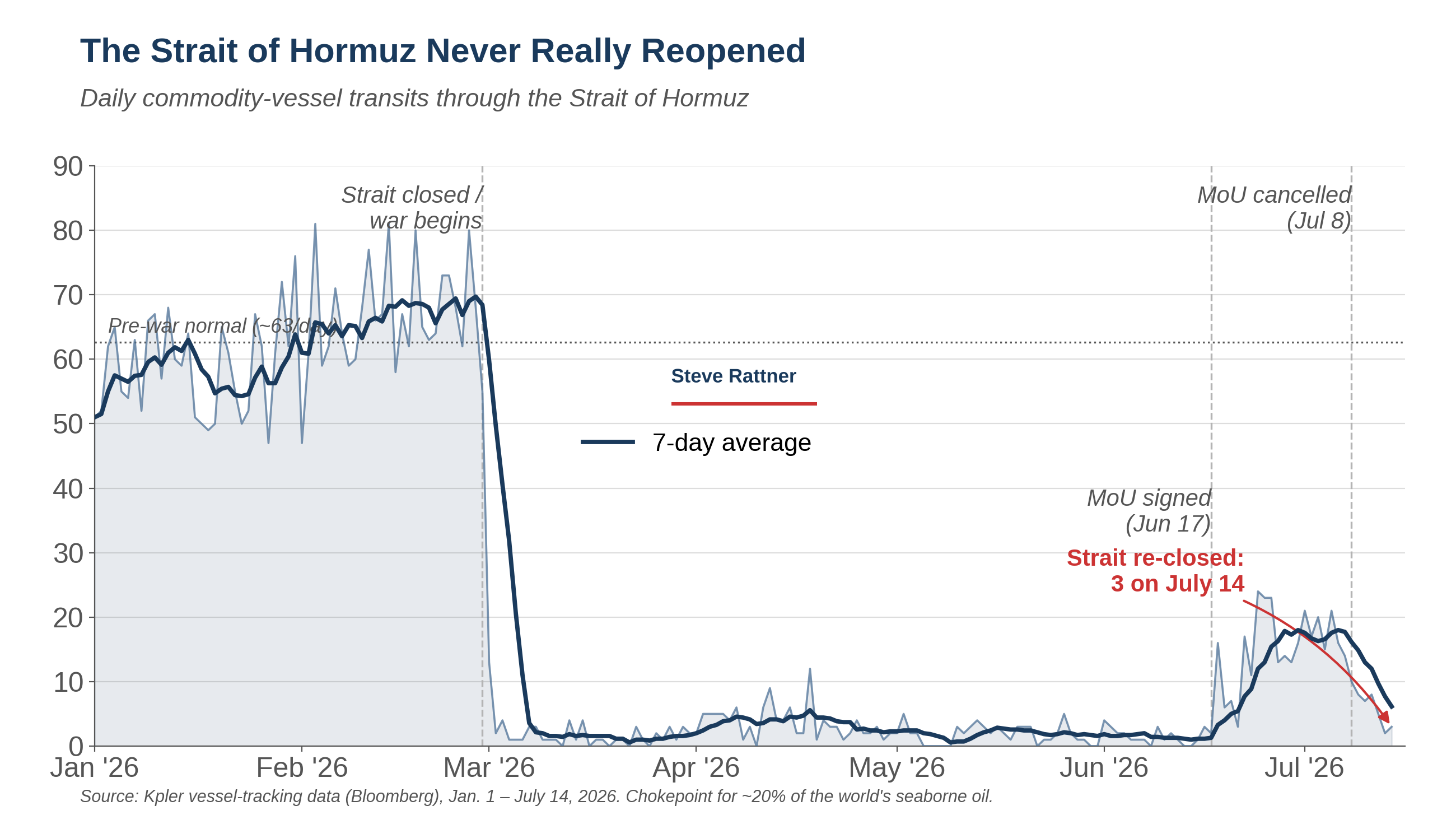

The prospects for oil prices and inflation remain, at best, uncertain. The Strait of Hormuz never really reopened during the short truce that the two sides negotiated, and now it is closed again. Global oil inventories remain low and a number of countries, including the United States, have drawn down significant amounts of their strategic petroleum reserves.

That has led financial markets to once again revise expected oil prices. Before the war, crude oil averaged $72 a barrel. It then surged to $118 per barrel before declining all the way back down to $72 a barrel. Now a barrel fetches $85. More concerning, the market does not expect oil prices to decline to prewar levels for the foreseeable future. That’s because the Iran War currently seems to have no durable offramp, and even once the conflict is resolved, it will take months to rebuild transportation and energy infrastructure in the Gulf region.