Originally published in the New York Times

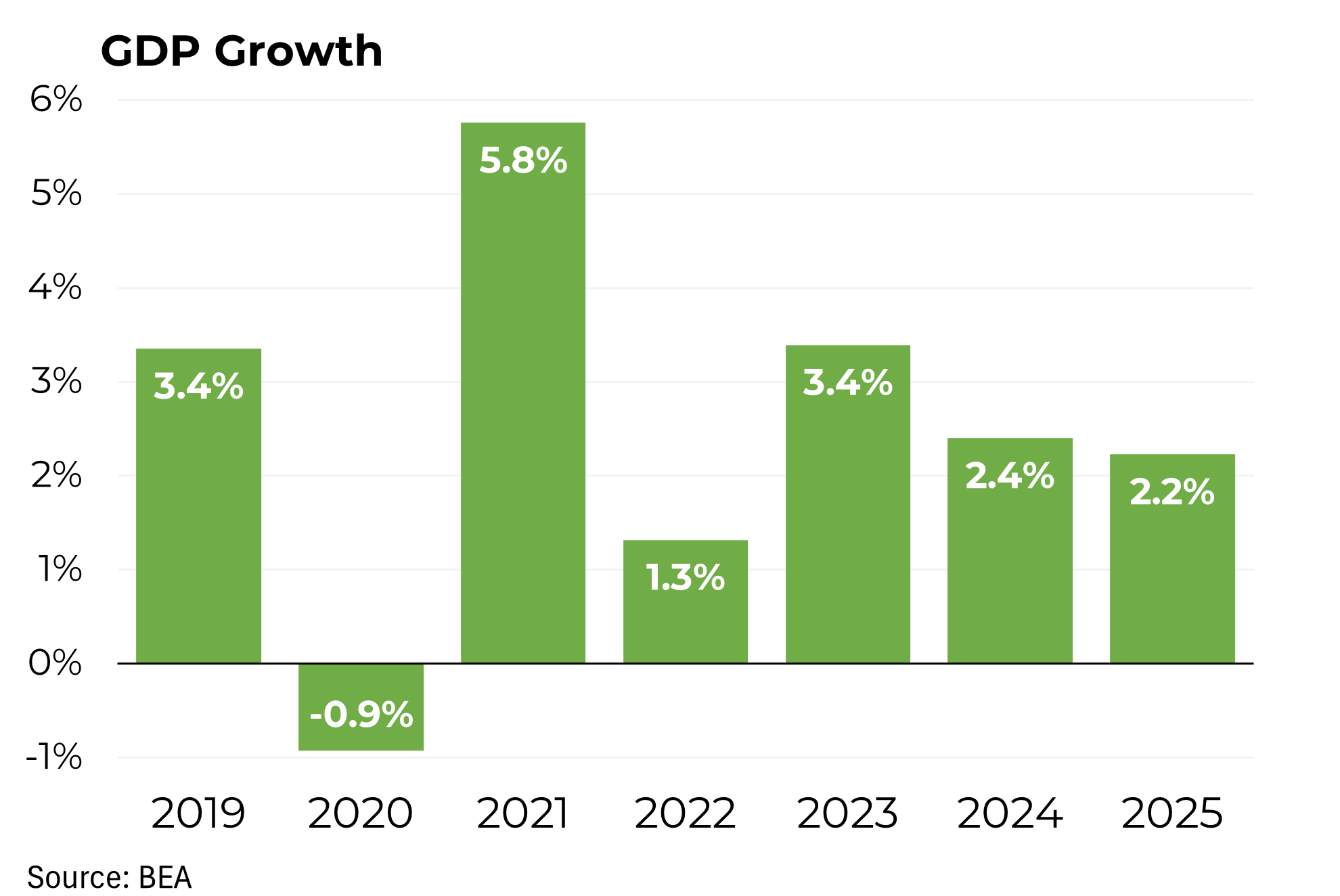

On its face, Friday’s announcement that the nation’s gross domestic product expanded at a 2.5 percent annual rate in the first quarter was good news, following as it did an only marginally positive result for the previous three-month period.

But, alas, that rosy headline figure masked disturbing signs: an economy whose recovery has failed to match the pace of past expansions may now be facing a deceleration in its own modest growth rate.

Start with the G.D.P. figures, which can be misleading because of temporary fluctuations in the inventories maintained by businesses. Adjusted for those changes, the economy’s annualized growth rate shows a steady deceleration over the past three quarters, from 2.4 percent to 1.9 percent to 1.5 percent.

That’s on top of a highly disappointing employment report for March, when only 88,000 new jobs were created, compared with an average of 197,000 for the previous six months.

And other economic measures — ranging from retail sales to the index of leading economic indicators — have begun to display softness and even declines. All told, at a minimum, we have entered yet another spring slowdown.

Perhaps it will prove transitory, as the pauses of the past three years have been. But worrisome signs suggest that this time may, indeed, be different.

For one thing, hourly wages, after adjustment for inflation, haven’t budged in more than three years. That’s unusual during an ostensible period of recovery, particularly from such a vicious recession.

Without higher incomes, consumers can’t expand their purchases (at least not without dipping into their savings).

Meanwhile, Washington’s budget wars have thus far produced a fistful of undesirable policy changes. Instead of thoughtful reforms — particularly to programs like Medicare and Social Security — to begin to bring the nation’s long-term debt under control, Congress has adopted a series of meat-ax measures.

While that has shrunk the federal deficit significantly — this year, the deficit is likely to come in at around $775 billion, compared with $1.1 trillion in the previous year — the sudden contraction is likely to slow the economy further, cutting the growth in America’s economic output this year by about 1.5 percentage points. Using basic yardsticks, that measures out to 1.5 million fewer jobs.

Finally, the weak world economy has knocked one American strategy for ratcheting up growth — faster increases in exports — badly off the rails. Just three years ago, United States exports were expanding at a 27 percent annual rate; today they are barely growing, and sales to Europe’s hard-hit economies are declining.

To be sure, unlike Europe, where countries have faced double-dip recessions (and, in some cases, the prospect of a triple-dip), the United States is highly unlikely to experience a similar fate.

Our economy still exhibits some signs of strength, like the gathering recovery in housing construction and home prices. That has been aided by a strong stock market, which has rebuilt the value of retirement accounts and other investments.

But without rising incomes (and with mortgage financing still constrained), Americans’ ability to buy new homes will remain limited.

Meanwhile, the stock market recovery has been built on the shaky pilings of higher corporate profitability that has resulted far more from cutting costs than from growing revenues. That’s not sustainable.

The challenges listed above, of course, would be substantial by themselves.

But the most worrisome aspect of our current economic doldrums is that we can’t expect any of the factors weighing on it to be self-correcting. For example, the lack of wage growth owes much to the continuing effects of globalization, a trend that has benefited the United States as a whole while hurting many workers.

Nor are the prospects bright for renewed expansion in Europe, or for a resumption of the meteoric growth rates we once saw in emerging market nations, particularly in China.

Were Washington functional, policy makers could significantly ameliorate these effects. First and foremost, Congress could adopt budget policies that would accomplish more thoughtful, more gradual — and yet, ultimately, more substantial — deficit reduction.

Instead of deep, across-the-board cuts in many important investment programs, ranging from infrastructure to research and development, we need to protect those initiatives while adjusting our social welfare programs to live within our means and protect the truly needy.

To address the effects of globalization, so much more can be done in education and training to prepare workers for the skilled jobs that play better to America’s strengths.

Congress would be doing the American people a service if it came together to tackle these more consequential questions, and not just the problem of air-traffic delays.