While the risks from President Donald Trump’s decision to attack Iran have rightly focused on the strategic and human risks, another important concern is the potential impact of the war on the world’s energy supplies, principally petroleum.

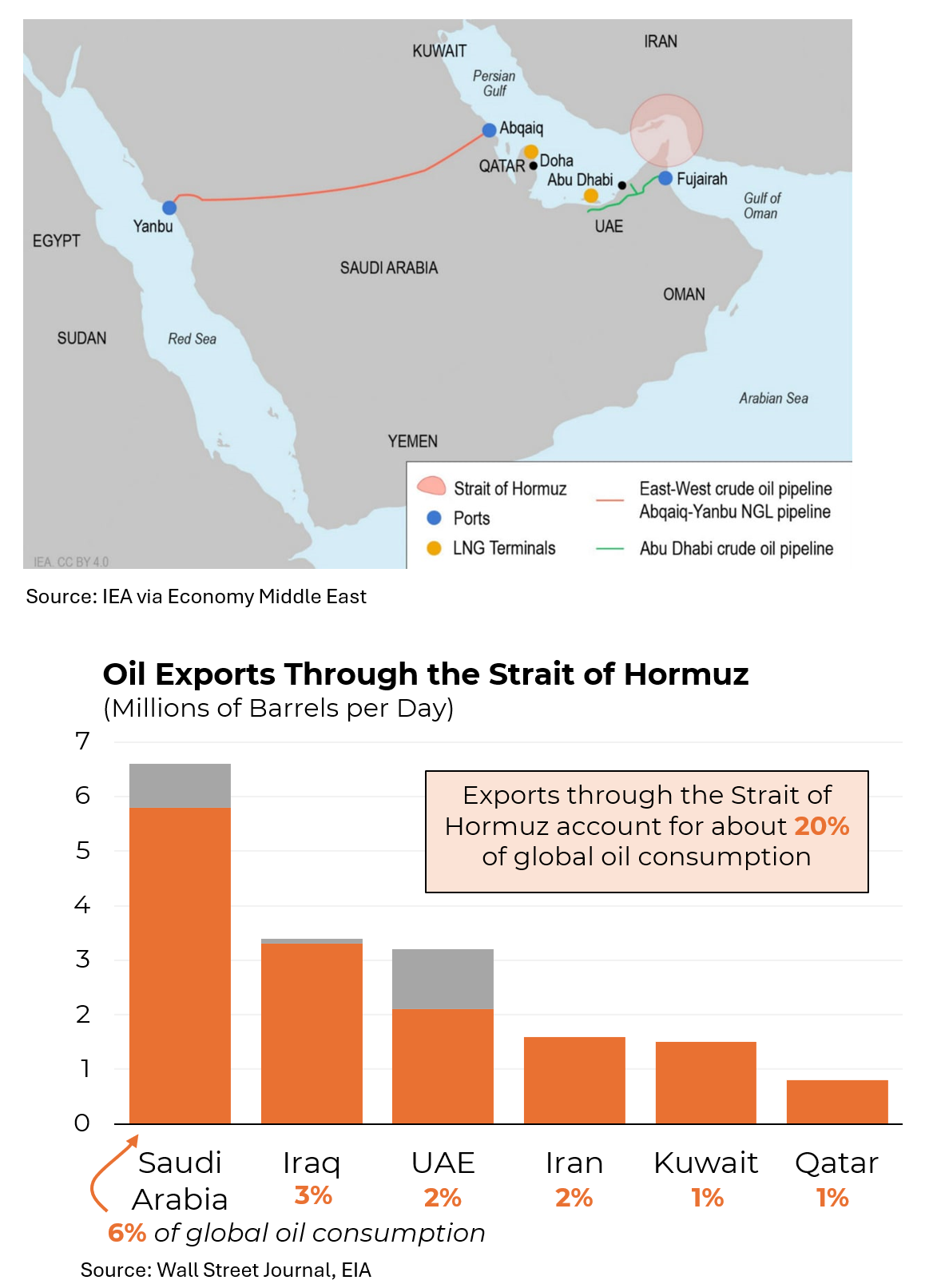

We’ve known for decades that a war involving Iran could result in the closure of the Strait of Hormuz, a 22 mile or so chokepoint with just two shipping lanes, each about two miles wide. As its northern neighbor, Iran is well positioned to use its weaponry to endanger ships attempting to traverse it. Consequently, maritime traffic through the Strait has essentially ceased.

That is hugely consequential. About 20% of the world’s oil (and a significant amount of liquified natural gas) passes through the Strait, including most of the oil produced by Saudi Arabia, Iraq and the United Arab Emirates. While there are pipelines across Saudi Arabia and the U.A.E. to avoid the Strait of Hormuz problem, these pipelines are already being partially utilized and in any event, don’t have nearly the necessary capacity.

As a result, storage is filling up throughout these countries and Iraq has already begun reducing production.

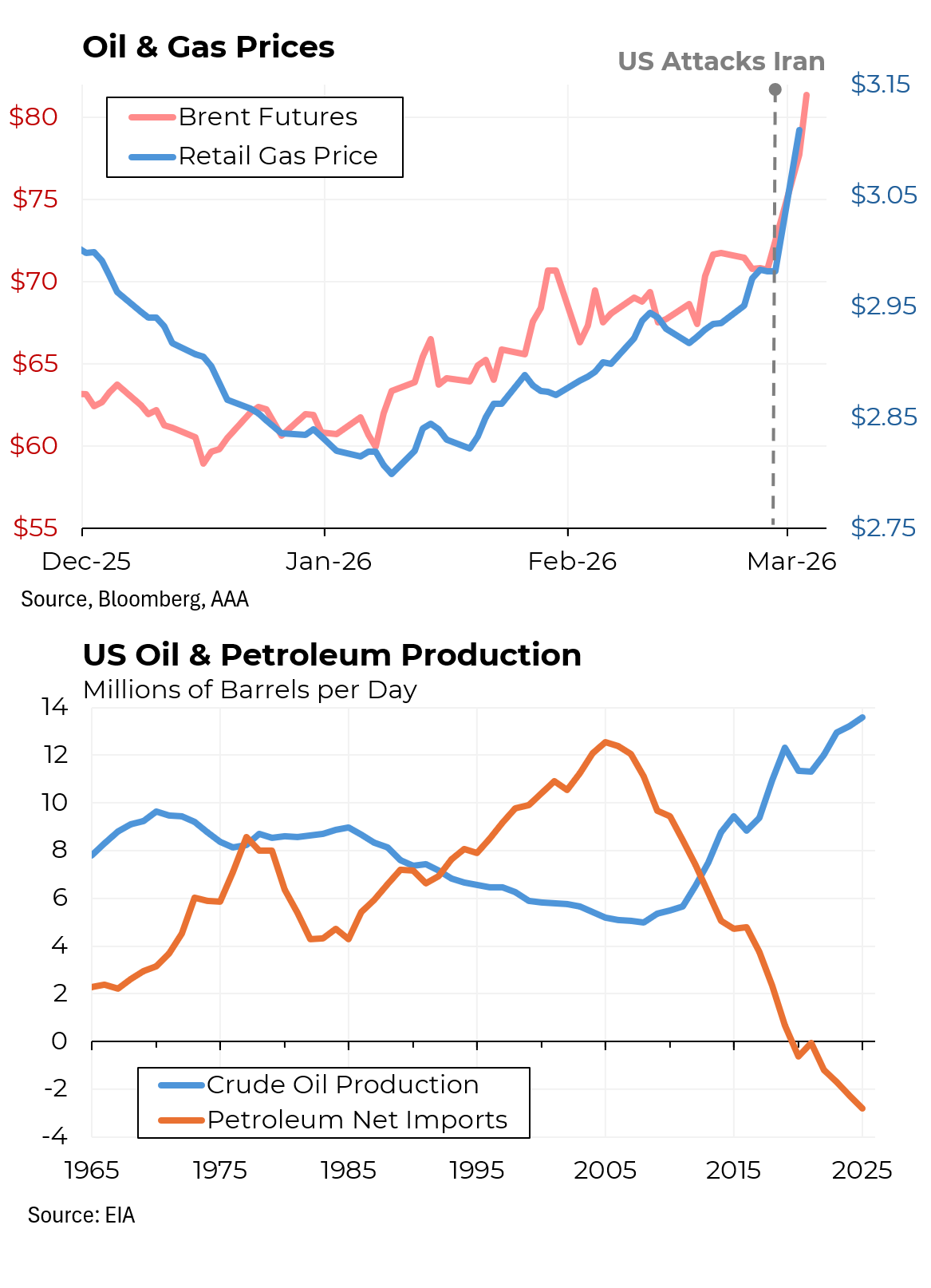

These realities have already caused oil prices to jump, to $81 a barrel for Brent crude, the benchmark grade, from $72 before the attack began. And gasoline prices, which had already begun to increase as the summer driving season approaches, also rose meaningfully. The American Automobile Association pegged the average price of gasoline at $3.11 per gallon, up from $2.98 last week. As there are 42 gallons in a barrel, each $1 per barrel increase in the price of crude oil translates into about 2.5 cents a gallon.

Not only will gasoline prices be higher but so will other petroleum products, such as home heating oil and jet fuel. Natural gas prices will also rise.

To be sure, the United States is in a far better position to weather this storm than it was during some past supply disruptions. Until just six years ago, the U.S. was a net importer of oil. Now we are the world’s largest oil producer and a significant exporter. That means that our overall economy benefits from higher oil prices. But that benefit is enjoyed by oil companies while consumers pay higher prices. (Because oil is easily transported, prices are similar around the world, after adjusting for transportation costs.)

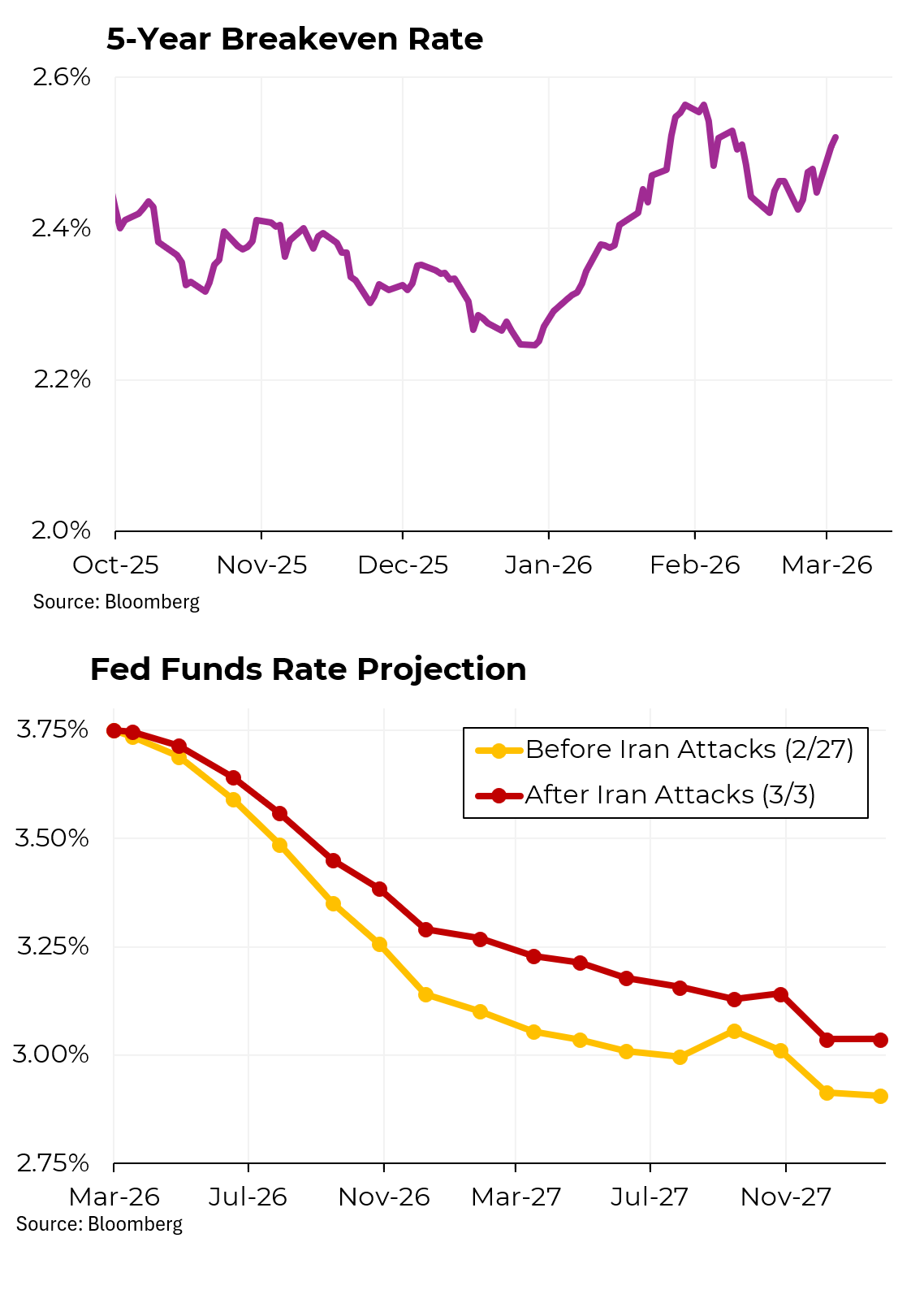

Although it recovered from its lowest point during the day, the stock market still closed 1% below its Monday night level. Certainly the heightened geopolitical risk played a significant role. But at least as importantly, the prospect of higher oil prices adds to inflation concerns. Inflation expectations had already been generally rising since the beginning of the year; in the past two days, they rose by another 0.1%.

This has led financial markets to raise their forecasts for interest rates. While the Federal Reserve had been expected to cut rates by another 0.5% this year, now the odds are closer to assuming just a 0.25% reduction. Higher interest rates are the enemy of stock prices so that shift contributed to Tuesday’s weak market.