President Trump’s first address to Congress of his second term was a bit surprising in one respect (at 100 minutes, it clocked in at the longest Congressional address in recent history) and not surprising at all in a second: It was replete with lies and exaggerations. Some were familiar (like the idea that President Biden left the economy in poor shape – ours is the strongest in the developed world.) Others were less familiar.

Surprisingly, Trump repeated a series of ridiculous campaign tax proposals – no tax on Social Security receipts, no tax on overtime, no tax on tips and the like. None of those could happen under the budget resolution passed 9 days ago by the House of Representatives. Under that agreement – supported by all Republicans but one – provided for $4.5 trillion of tax cuts over the coming decade, just slightly more than is needed solely to extend the expiring tax cuts originally passed in 2017. Adding in Trump’s other tax cuts would bring the total to $7.8 trillion.

And as he did in his first term, the president pledged to balance the budget. That’s also absurd, given that the House budget resolution would add $2.8 trillion of new deficits, on top of the over $20 trillion of debt that would already be incurred under current law. (Note that the president said in his first campaign that he would pay off all the federal debt by the end of his second term. Nor did the 2017 tax cuts come close to paying for themselves, as he had also promised.)

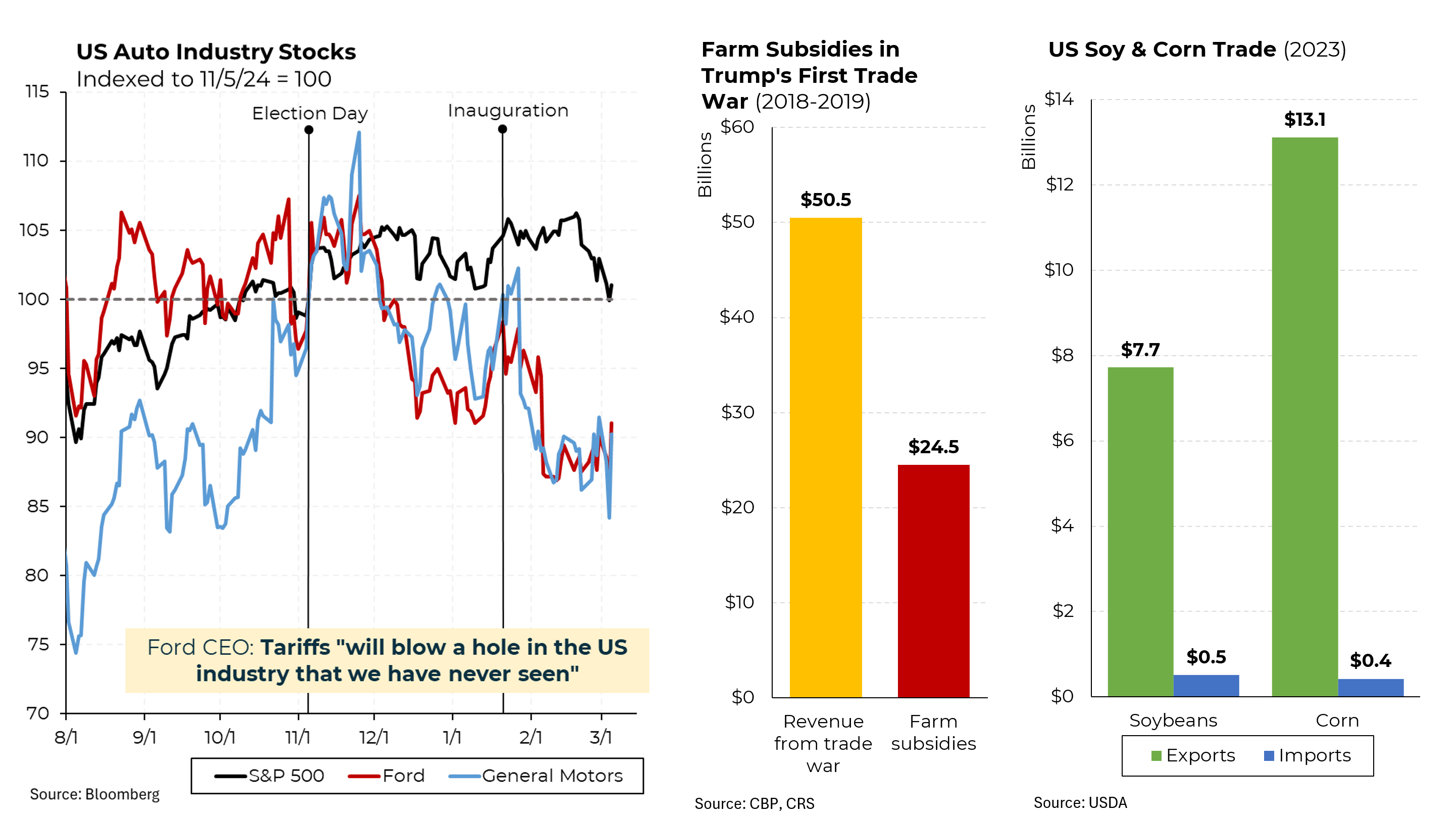

While Trump hardly mentioned tariffs in his speech, they are very much a major news topic as his latest round of levies caused the U.S. stock market to plunge. Autos are particularly affected as we import about 40% of our vehicles, many of which are produced by General Motors and Ford in factories operateed in Mexico and China. Moreover, because of the pre-existing free trade agreements with Mexico and Canada, parts and subassemblies often cross the border multiple times in the course of manufacture. Just since the inauguration, GM stock has dropped 10% and Ford stock has fallen 7.5%. Tariffs “will blow a hole in the US industry that we’ve never seen,” Jim Farley, the Ford chief executive said. Perhaps because of that, yesterday, Trump paused the auto tariffs for one month.

Then there are the farmers. The U.S. is the largest agricultural exporter in the world. In his first term, because of the pain felt in the farm belt from retaliatory tariffs, Trump ended up turning over almost half the $50 billion of total tariffs collected in 2018 and 2019 to farmers. Contrary to what he said Tuesday night, farmers have no domestic market in which to sell the exports that will presumably fall off. We import little of the main cash crops of soybeans, corn and the like.

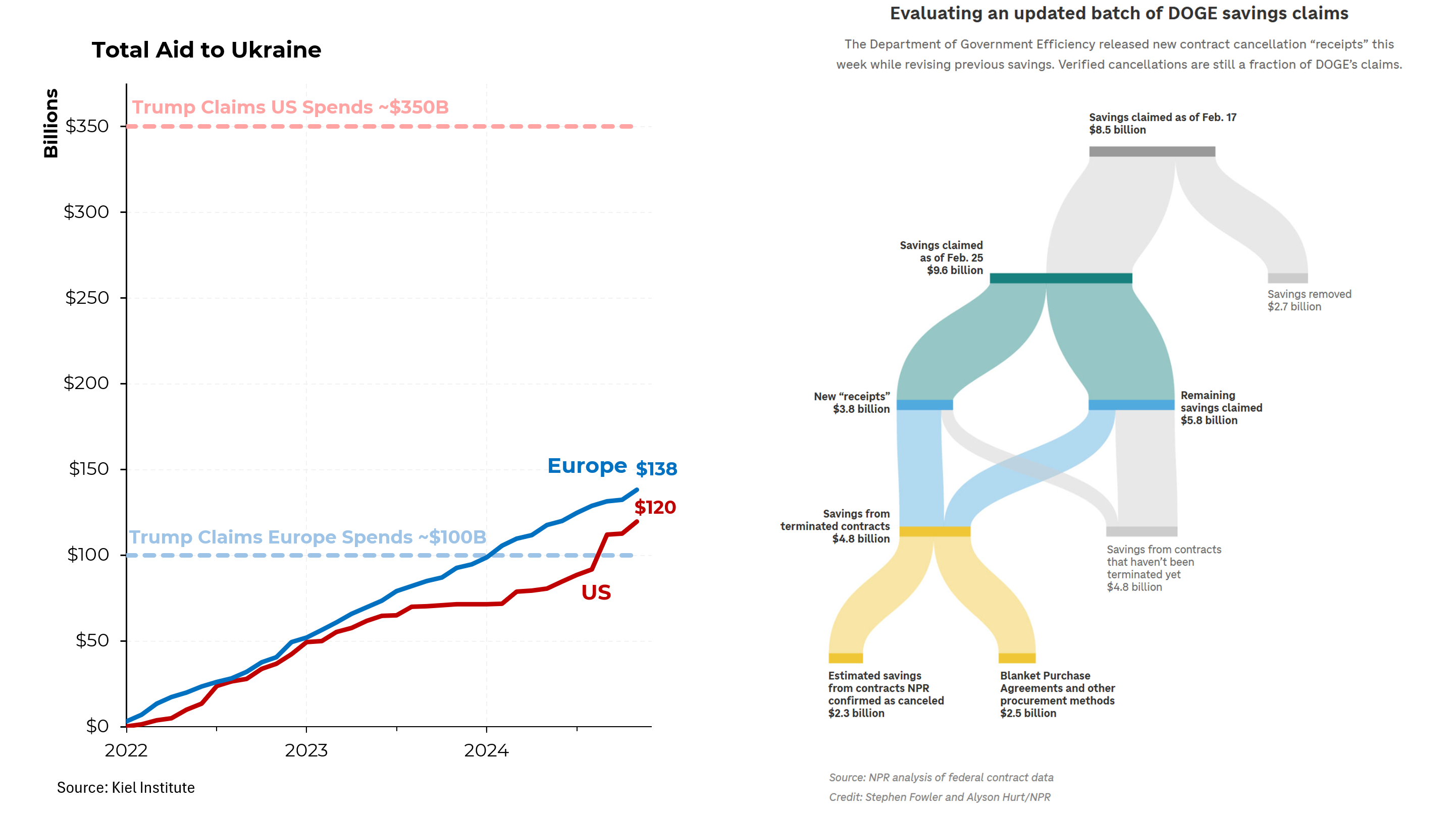

You’d think that by now, Trump would understand that the figures he keeps citing about Ukrainian aid are just wrong. No, Europe has not contributed more than we have. And no, we have not sent anything like $350 billion. We have still sent more than Europe (although after last week’s Oval Office events, that may be changing.)

And then there’s DOGE. Trump claims that his team has found hundreds of billions of dollars of fraud (and he provided an endless list, mainly of small items). That may have come as news to Elon Musk. His DOGE team initially claimed $8.5 billion. But then it turned out that many of those savings didn’t exist for one reason or another so now DOGE is down to $4.8 billion (a long way from “hundreds of billions.” And let’s not forget that $4.8 billion is 0.07% of our federal budget of $6.75 trillion.