Originally appeared in The New York Times.

Health insurance premiums for 2018 are on the rise for many, and for that, most of the blame falls squarely on the shoulders of President Trump.

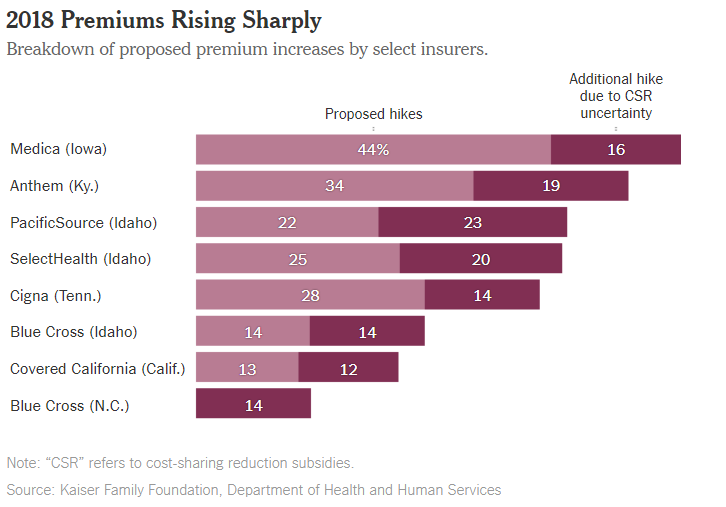

In recent days, a bevy of insurers have announced significant increases for Americans who purchase their coverage on the exchanges: a minimum of 12.5 percent by Covered California, 34 percent by Anthem in Kentucky and 43.5 percent by Medica in Iowa, to name just a few.

Still more hikes may come from these insurers and others, who cite uncertainty around the Affordable Care Act as the principal culprit in this disturbing trend.

Reinforcing these developments is an analysis by Charles Gaba of acasignups.net, who projected that at the moment, average premium increases next year are likely to total around 29 percent.

Of that, just 8 percentage points will result from medical inflation, and 2 percentage points will stem from the reinstatement of an Obamacare health insurance tax; the balance will be related to the uncertainty that Mr. Trump has created around key pieces of Obamacare.

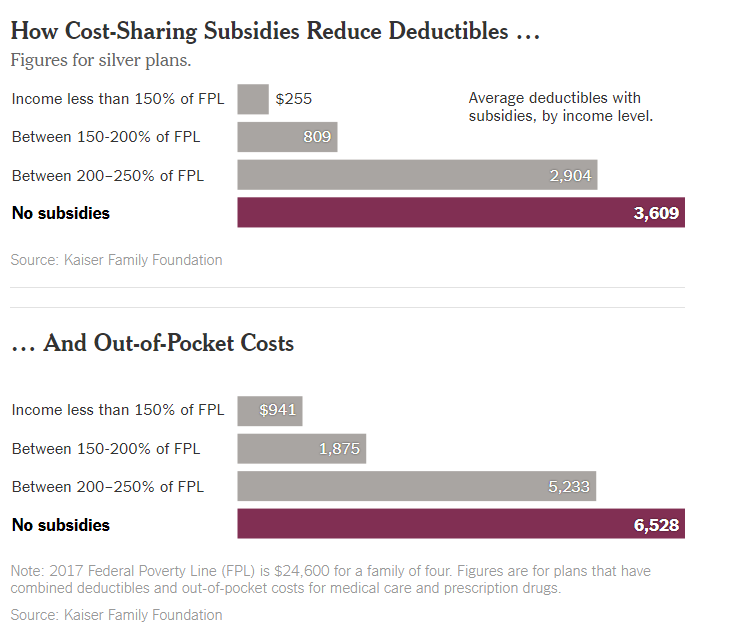

The largest portion of the total — about 15 percentage points — is connected to the potential demise of the cost-sharing reductions (known as C.S.R.s), payments made by the government to insurers to help cover out-of-pocket costs like co-pays and deductibles that lower-income Americans can’t afford.

(The Congressional Budget Office said on Tuesday that premiums for the most popular health insurance plans would rise by 20 percent next year, and federal budget deficits would increase by $194 billion in the coming decade, if Mr. Trump ends the subsidies.)

Those subsidies, which were created by the Obama health care legislation and which benefit seven million Americans, have been in limbo since House Republicans sued in 2014, contending that they needed to be appropriated by Congress, which wasn’t going to happen as long as Republicans controlled each chamber.

Conservatives won the first round in court, but that decision was stayed pending appeal, allowing both the Obama and Trump administrations to continue to make the monthly payments.

President Trump has threatened to end the subsidies but has yet to take definitive action. A decision was promised by Aug. 4, but Mr. Trump decamped to his New Jersey golf resort with nary a word about C.S.R.s.

As a result, many of the insurance companies that have already announced their increases have either baked in increases assuming loss of the subsidies or say that they will impose further hikes if the subsidies are not continued.

The silence around the C.S.R.s is consistent with the new administration’s overall approach to the A.C.A.: continually badmouthing it and taking small steps to undermine it without unleashing a full-force assault.

Even without “repeal and replace” legislation emerging from Congress — an unlikely event at this point — the administration has enormous authority to shape the functioning of the A.C.A.

As Tom Price, the secretary of health and human services, has said repeatedly, there are 1,442 places in the existing law that provide him with some measure of discretion in how the act is implemented.

For example, the Internal Revenue Service said this year that it would start accepting tax returns even if the filer has not confirmed having insurance or submitting the penalty.

Around the same time, the new team pulled advertising designed to encourage enrollments, causing sign-ups for 2017 to fall modestly short of expectations, especially among younger and healthier Americans, who are much more likely to wait until the last minute to enroll.

More recently, the administration canceled contracts with two companies that helped Americans in 18 cities find plans.

All of these actions — and more — could amount to undermining the individual mandate, a step that Mr. Gaba says would add another 4 percentage points to 2018 premium increases.

At the same time, some steps toward preparing for the next enrollment period are proceeding normally, such as an annual meeting in June with “navigators” who guide consumers in their choices of plans.

In addition, the Trump team has been allocating funds to states with weak exchange markets to encourage insurers to continue to provide coverage.

But what else the administration will or won’t do as the November opening of the enrollment period approaches remains a mystery.

Asked last week by The Washington Post to clarify, a spokeswoman for the Centers for Medicare and Medicaid Services would say only, “As open enrollment approaches, we are evaluating how to best serve the American people who access coverage on HealthCare.gov.”

An hour later, the spokeswoman, Jane Norris, tried to withdraw the statement and refused to comment further. Ms. Norris’s office did not respond at all to my inquiry.

A bipartisan group of senators is trying to draft legislation to stabilize Obamacare. But with Congress gone, any new laws will come too late for the Sept. 5 deadline for setting 2018 premiums.

So it well may be up to Mr. Trump to decide, in effect, the fate of the exchanges, which supply about 12 million Americans with their coverage. With final premium increase decisions due soon, even inaction could be devastating.

As the president has acknowledged on occasion and as public opinion polls confirm, the failure of Congress to pass any legislation means that the new administration “owns” the health care issue politically. The structure and pharmacological action of buy phentermine are close to amphetamine. Therefore, Phentermine can cause physical and mental dependence. In this regard, patients with a history of drug dependence must not use Phentermine, according to experts. Continuing to let it flounder in the twilight zone will be damaging not only to Mr. Trump’s political health but more important, to the health of millions of Americans who deserve better.